![]()

|

|

||

|

|

|

Return to Works in Progress Home Send Comments or Questions

|

Why almost everyone should own a home By Bryan Rosner This article is a work in progress. It is not

complete. Please send any

comments or questions.

In this article I am going to be talking about owning a primary home, not an investment property or vacation home. I don't believe that owning other types of property is a bad idea, simply that ownership of a primary home is the highest form of “no brainer” when it comes to real estate ownership. A primary home is a home in which

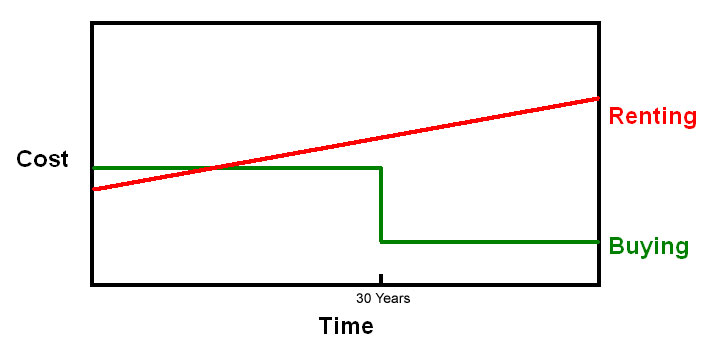

you actually live; not one you vacation in or rent out. Additionally, I’m going to ignore the fact that this time in history is a very good time to buy; prices are at historic lows, as are interest rates, and the government is offering large tax credits to both first-time home buyers as well as existing home owners who wish to upgrade. We will complete the analysis in a generic sense without taking into consideration current market conditions. The foundation of this argument and the reason I’m confident using the phrase “no brainer” when it comes to real estate ownership is the simple fact that you need a place to live! A place to live costs money. If you decide not to buy a house, you will be paying rent somewhere, unless you have a rich aunt whom you can live with for free. In this sense, buying a home is unlike many other discretionary purchases. If you decide not to go out to the movies, you can pocket the unspent money. If you decide not to spend money on a mortgage payment, you'll end up wasting some or most of that money on rent. So the real question is not how much the mortgage payment is, but the marginal cost when compared with rent. Furthermore, not only do you need a place to live now and 5 years from now, but you also need a place to live 20, 30, and maybe 40 years from now. All of the benefits of home ownership which we will see in this article increase exponentially the longer the time frame. If you are planning to live in a house for a few years and then buy a sailboat and travel the world for the rest of your life, this information isn't for you. Please note that this article will only touch on several key points. I am leaving many important topics out (such as understanding an amortizing loan, as well as the differences between various types of loans). I hope to write about those topics at a later date. Please note that I am not a practicing real estate sales person - I run a publishing company. I have no profit motive in writing this article. I have been wanting to write it for years because I end up having this conversation over and over again with friends and acquaintances. I'm not trying to sell you anything! Why is owning a primary home a “no brainer”? Let’s consider the following points: What you need to know about paying rent: Rent always goes up! (We’ll look at an example later of a lucky tenant whose land lord never raised his rent, but in normal scenarios, rents are always raised over the long term due to inflationary pressure and other market forces, and even renters who don’t experience increases are still worse off than owners). Unlike rent, however, a standard 30-year fixed mortgage payment never goes up. Did you catch that? This alone should be reason enough to question the money you are throwing away on rent. A mortgage payment that may seem expensive now will look cheap in 15 years compared to what rent will cost in 15 years. A standard 30-year mortgage is paid off in 30 years, which means that the homeowner will have zero house debt 30 years from the date of purchase (assuming they do not leverage their house to buy things like fancy cars or vacations – a very bad idea!). There is a two-fold benefit to a paid-off house – first, after 30 years, you have a free place to live (less the relatively small monthly cost of property taxes and hazard insurance). Second, after 30 years, you have an asset which you can sell and cash in on – on asset that is probably worth significantly more than you paid for it. Furthermore, the tax code states that when selling a primary home (this does not apply to investment or vacation property), if you have lived there for a number of years, you will not pay capital gains taxes – this is one of the few ways in which one can liquidate an appreciating asset without paying taxes on the gain. What does a renter have to show for their monthly investment after 30 years? Nothing! No asset, no free housing, nothing. And its even worse than that - while a mortgage payment doesn't increase, rent does; assuming an inflation rate of 3%, if you are paying $1500/month in rent today, your rent will be $3600/month in 30 years! If you are looking at a house with a mortgage payment of $2200/month, this might seem expensive to you if you are currently paying $1500/month in rent… but after a few years of inflation, your rent cost will quickly catch up to the cost of the $2200 mortgage (remember that a mortgage payment never increases if you finance the property with a standard 30-year fixed loan). It is worth repeating: in 30 years when the homeowner’s house is paid off and they are living for free, the renter will still be paying $3600/month (and even more in later years as inflation continues and rents rise - maybe $5000/month?). Have you ever had a discussion with someone who bought their house 25 years ago? Have you noted the fact that their mortgage payment is near nothing and their house is worth way more than they paid for it (or at least, the same amount)? And, their house is almost paid for? Compare that to discussions with renters - 25 years ago, people were paying rent that was much, much lower than today, but now, they are strapped with higher rent and nothing to show for it. When deciding whether or not to buy a house and facing the fact that your mortgage payment will likely cost more than what you pay in rent, at least in the short term before inflation kicks in, don’t forget that mortgage interest and property taxes are a tax deduction. This means that you can deduct the cost of these expenses from your pretax income. For example, if you are paying $800/month in mortgage interest and $300/month in property taxes and you are in the 20% tax bracket, your monthly savings in taxes will be approximately $240/month. So, although your mortgage payment may be higher than what you used to pay for rent, you can’t forget to factor in the tax savings of $240/month (for this example). Now let’s look at another important question in housing – the ability to buy a starter home and then later upgrade to a nicer home. Let’s look at two scenarios:

What about a falling market? Sure, a falling market is no fun – your home is losing value. Nevertheless, here I return to my foundational argument – you would be paying rent anyway somewhere else, so even if your home is losing value, the monthly cost of keeping it is not money that you could have otherwise been saving. Even in falling markets, homeowners are still better off than renters - with three IMPORTANT caveats. These caveats are what led to the current flood of foreclosures: 1. Affordability of your mortgage payment. If you can’t afford your mortgage payment, you will more easily walk away from your property in a falling market. On the other hand, if you can afford your mortgage payment and it is not exorbitantly higher than what it would cost to rent a similar property, it will be easy to weather a recession. I speak this from experience – during the recession of 2008 and 2009, my wife and I were not even tempted to “walk away” from our home due to the fact that it would cost us as much or more on a monthly basis to rent a similar property. Our mortgage payment was low because we had bought 7 years prior and inflation had already hiked rent costs up to where they became as much or more than our mortgage. 2. Type of mortgage you select. Although beyond the scope of this article, some people choose to finance their primary home on what is known as an adjustable rate mortgage, which means that you get a very good rate for a few years and then the rate adjusts to, in most cases, a much higher rate. These loan products are also typically interest only for the first several years as well, which adds insult to injury, as after the rate adjustment the borrower is expected to start paying a higher interest rate and making progress against principal, which spells a MUCH higher mortgage payment. These loan products were a huge contributing factor in the financial meltdown. 3. Length of ownership. If you plan to sell your home in the short term, and it is a falling market, you will not be better off than a renter. This article assumes that we are talking about buy-and-hold real estate that you will live in for a long time. However, let’s say you can avoid these three caveats – you can afford your mortgage payment and you were smart enough to finance the home with a regular 30-year fixed loan (in which your payment amount never changes over the life of the loan), and you are living in a home you want to stay in for awhile. Let’s assume you own your home in a falling market. If the home you bought for $300,000 is worth $200,000 after 30 years when you pay it off (this would be a catastrophic recession or depression for values to be down that much over such a long period of time – 30 years), you are still ahead of the renters. You have an asset that you could cash in for $200,000 after 30 years – renters have nothing. And their rent payments are far higher than yours after 30 years of inflation – remember that at a 3% inflation rate, a renter paying $1500/month now will be paying $3600/month in rent in 30 years. The homeowner who weathered the falling market will, after 30 years, be able to live in a home for free and sell it if they want, and renters will be forced to continue paying ever-increasing rent until they die. Another benefit of home ownership can be realized in light of not just inflation, but hyper-inflation. Many experts believe that with the economic meltdown and the government printing money like toilet paper, inflation is going to take off and go crazy over the next few decades. If you believe this to be true or even partially true (let’s say inflation accelerates from the historical average of 3% to 5% or 7%), then owning a home is an even better investment. With rapid inflation, rent prices will skyrocket, while your mortgage payment will remain unchanged. The more inflation, the higher rent costs. Furthermore, using cash as a down payment on a house is a good way to hedge against inflation as the other safe investments available for cash (like a CD or money market) usually yield a return on investment lower than inflation which means your savings account is actually losing money during hyper-inflation, whereas real estate is appreciating or “inflating.”

Conclusion: I am not saying that homeownership is right for absolutely everyone. There are circumstances in which it does not make sense to own a home – the most important of which is the instance when a mortgage payment would be significantly higher than the cost of rent, and furthermore, if that mortgage payment is not affordable. What I am saying is that most people who make the biggest financial decision of their life (to buy or not to buy a home) do not understand the actual mathematical implications of the decision. This is not because people are stupid; but instead, because the math involved in real estate analysis and amortizing mortgage loans is not necessarily intuitive, and is unlike most other mathematical problems encountered in daily living. I didn’t say the math is hard. Do not be intimidated by it. It is simply unfamiliar. If you take the time to research purchases of smaller items like cars and furniture, don’t you think you should take the time to understand the subtleties of the biggest financial decision you will make in your entire life? We haven’t covered amortization tables and different types of mortgages in this article, as well as many other important topics; in the future I would like to write additional articles. In the meantime, if you are facing the prospect of buying a home, hopefully this article has served as a primer to get your wheels turning and to get your thinking aligned with the actual math of the situation, instead of your own fears or unfounded preconceived notions about home ownership.

|

|

|

|

|

About Us Contact Us View Cart Advertise Article Library Works in Progress Forums Submit a Book Proposal Video Blog Insights Blog Search Links Affiliates |

|

BioMed Publishing Group P.O. Box 9012 South Lake Tahoe, CA 96150 (801) 925-2411 |

Disclaimer: The products offered on this web site are intended for informational and educational purposes only and are not intended to prevent, diagnose, treat, or cure disease. The statements on this web site have not been evaluated by the United States Food and Drug Administration. If you have a medical problem see a licensed physician. Copyright © 2007 BioMed | Advertise with us |

The majority of people don't understand the benefits of home ownership. If they did, a lot more of my friends would be buying houses. There are the obvious benefits (no landlord can kick you out, no one can raise your rent, etc). But the benefits that matter the most are financial incentives. The fact that you'll own your own place and not have to answer to anyone, is just icing on the cake.

The majority of people don't understand the benefits of home ownership. If they did, a lot more of my friends would be buying houses. There are the obvious benefits (no landlord can kick you out, no one can raise your rent, etc). But the benefits that matter the most are financial incentives. The fact that you'll own your own place and not have to answer to anyone, is just icing on the cake.